Macro Summary 15.11.2021

Macro Summary 15.11.2021

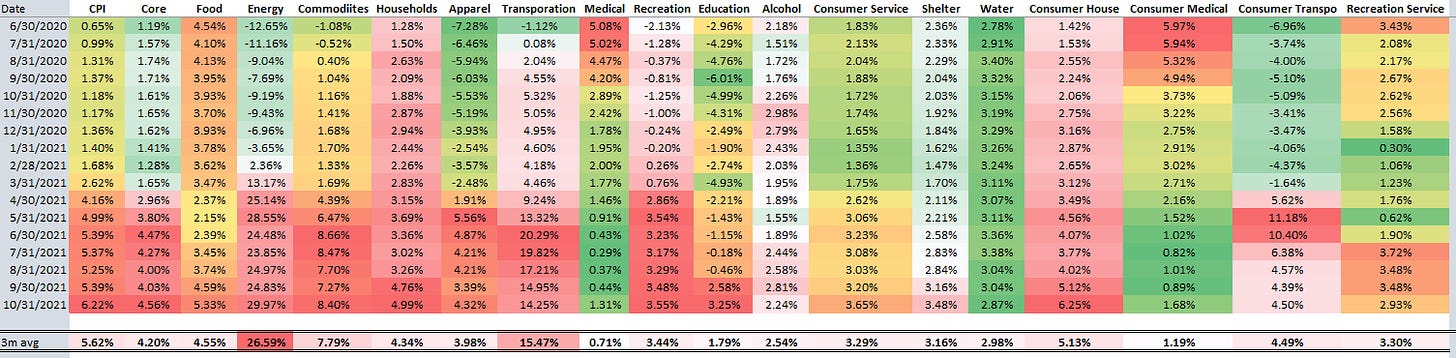

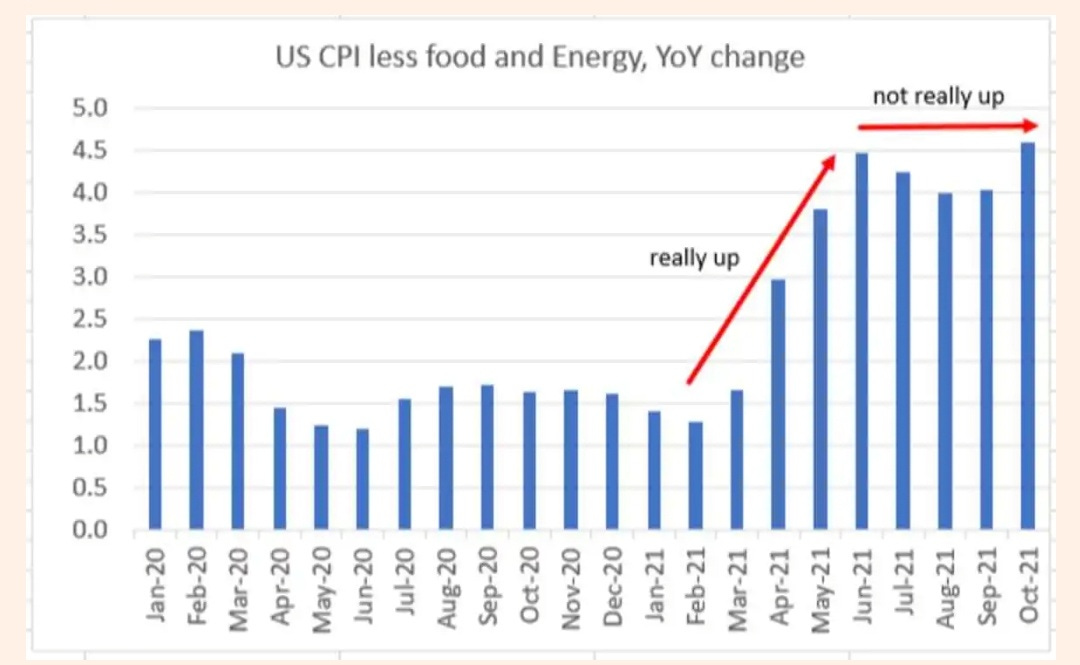

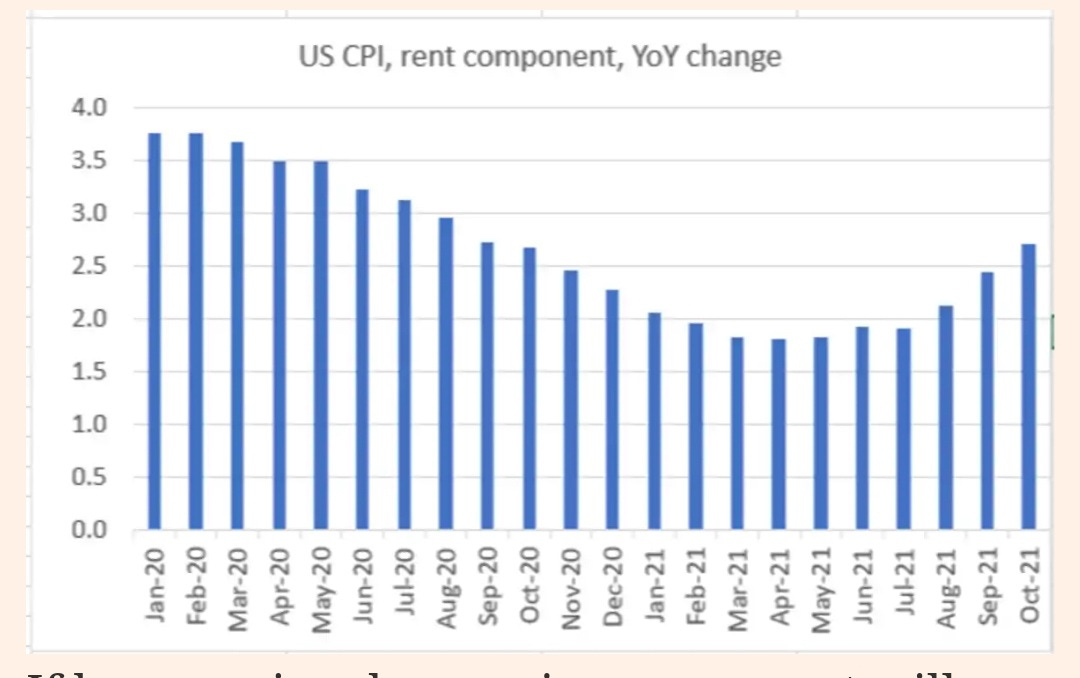

Inflation getting broad

Introduction: The week has been dominated by the CPI numbers and consequent worries about inflation. CPI showed a more broad based inflationary increase across more than just energy and cars (chip dependent). Markets are more concentrated than before on possible rate hikes. Add rising corona numbers and deaths into the mix and uncertainty seems to be more present than over the summer. Company earnings however stay strong and forward guidance, even when shadowed by a new wave, is positive. It is more expectable that this corona wave is likely not going to hurt the economy as bad as the previous one, especially now with adapted people, companies, treatments and new medicine.

Markets -- Seeking Alpha

U.S. Indices: Dow -0.6% to 36,100. S&P 500 -0.3% to 4,683. Nasdaq -0.7% to 15,861. Russell 2000 -1.1% to 2,411. CBOE Volatility Index -1.2% to 16.29.

S&P 500 Sectors: Consumer Staples -0.3%. Utilities -0.9%. Financials +0.1%. Telecom -2.1%. Healthcare +0.2%. Industrials -0.4%. Information Technology -1.%. Materials +1.8%. Energy -1.4%. Consumer Discretionary -3.6%.

World Indices: London +0.6% to 7,348. France +0.7% to 7,091. Germany +0.3% to 16,094. Japan 0.% to 29,610. China +1.4% to 3,539. Hong Kong +1.8% to 25,328. India +1.% to 60,687.

Commodities and Bonds: Crude Oil WTI -0.7% to $80.72/bbl. Gold +2.8% to $1,867.9/oz. Natural Gas -13.3% to 4.78. Ten-Year Treasury Yield -0.9% to 130.67.

Forex and Cryptos: EUR/USD -1.05%. USD/JPY +0.46%. GBP/USD -0.56%. Bitcoin +3.7%. Litecoin +25.2%. Ethereum +2.7%. Ripple +2.4%.

Indicators:

Inside the stock market

Communication, Health Care & Utilities are underperforming.

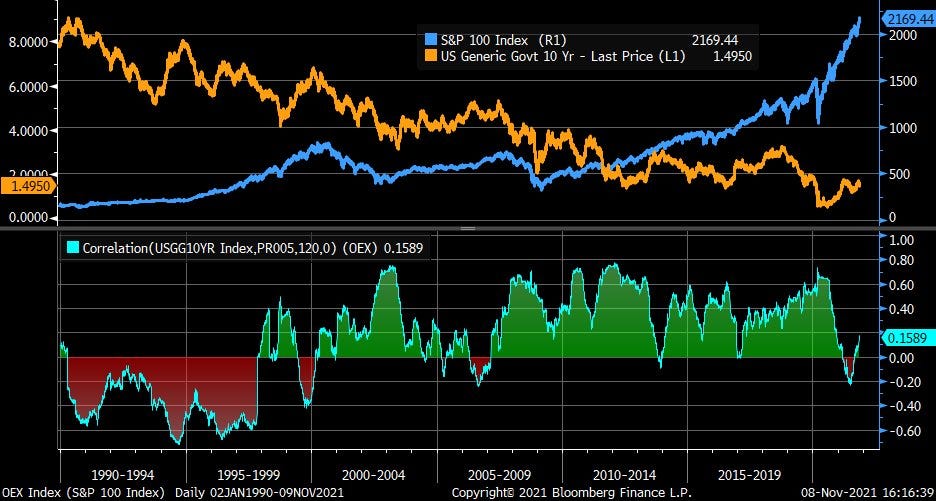

Yield Curve

US10Y - DE10Y spread is breaking out to the top.

US30Y held key support level of 1.80. US02Y is still rising.

5-30 curves are still flattening aggressively in Europe and the US

The MOVE Index is at April 2020 highs, while the VIX is keeping low levels.

Credit

All the major metals are rebounding, with Gold leading.

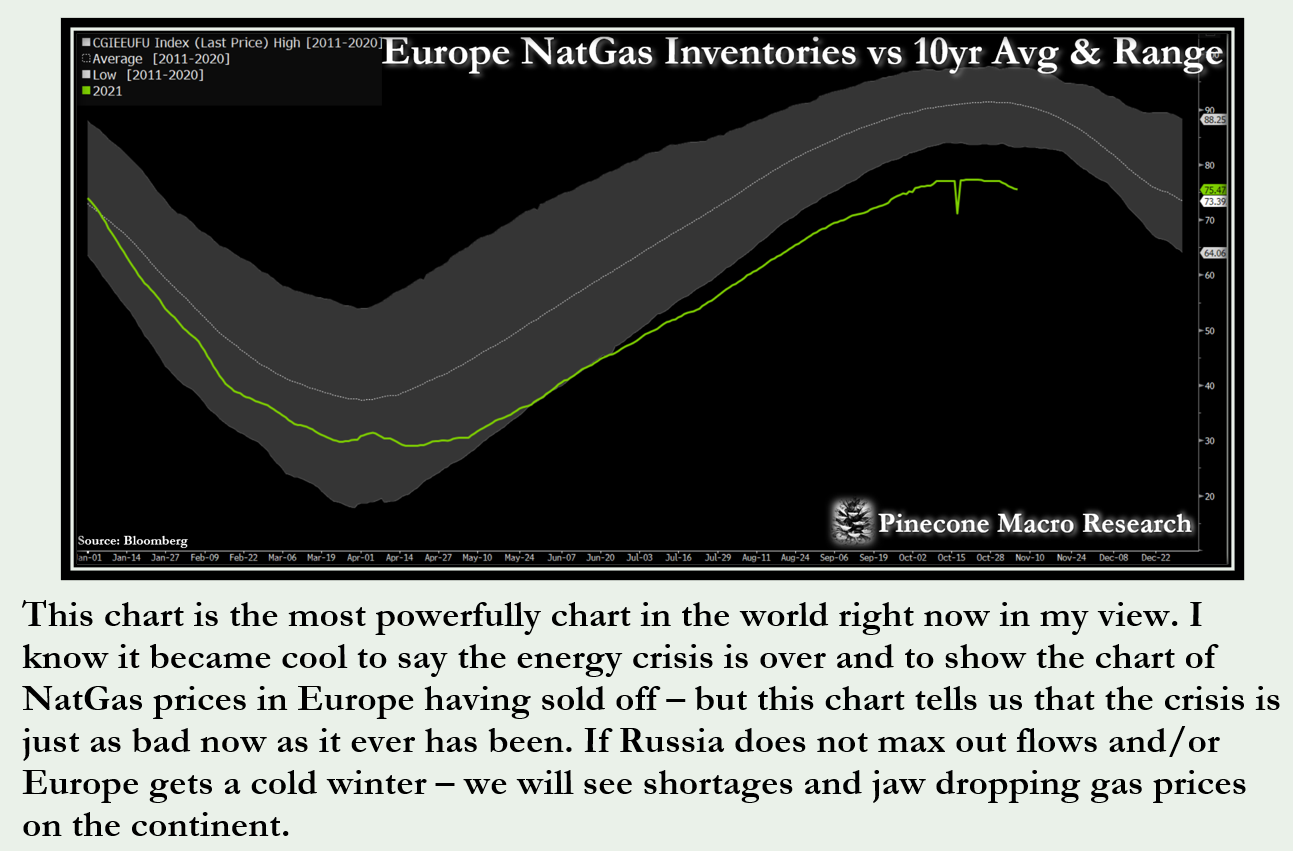

Natural Gas is falling below 5, Oil is also correcting. The spread between the two is also rebounding to the upside.

Soybean Meal and Soybean Oil look like they are starting to follow Wheat and Oats to the upside again.

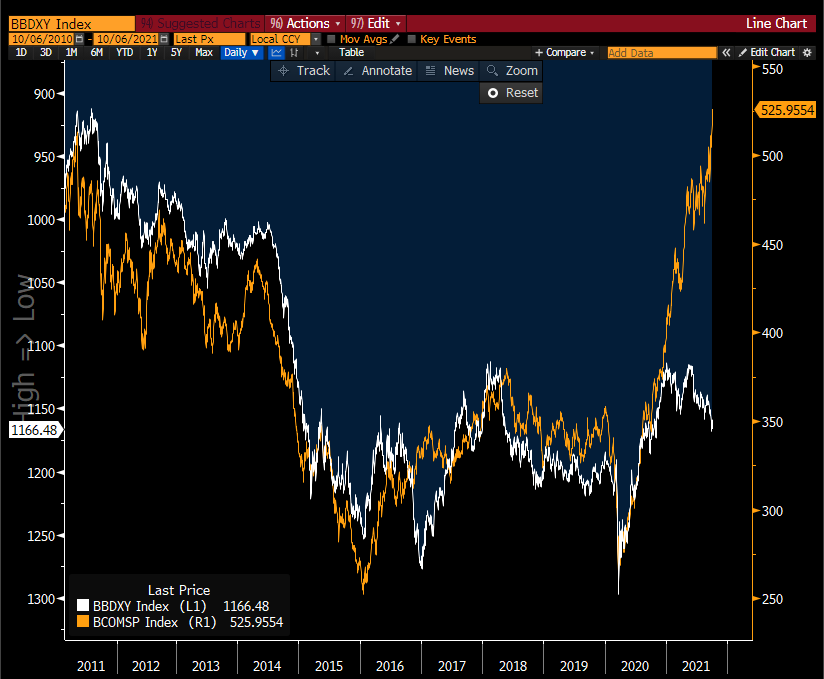

USD is staying strong, but British Pound and Euro Futures are at key support levels.

Baltic Dry is below 3000 again.

Economics & Major News

US PPI MoM Oct came out as expected at 0.6.

Germany ZEW Economic Sentiment Index for October came out positive at 31.7 vs. 20 expected.

Chinese Inflation came out high, but close to expectations at 1.5% vs. 1.4%

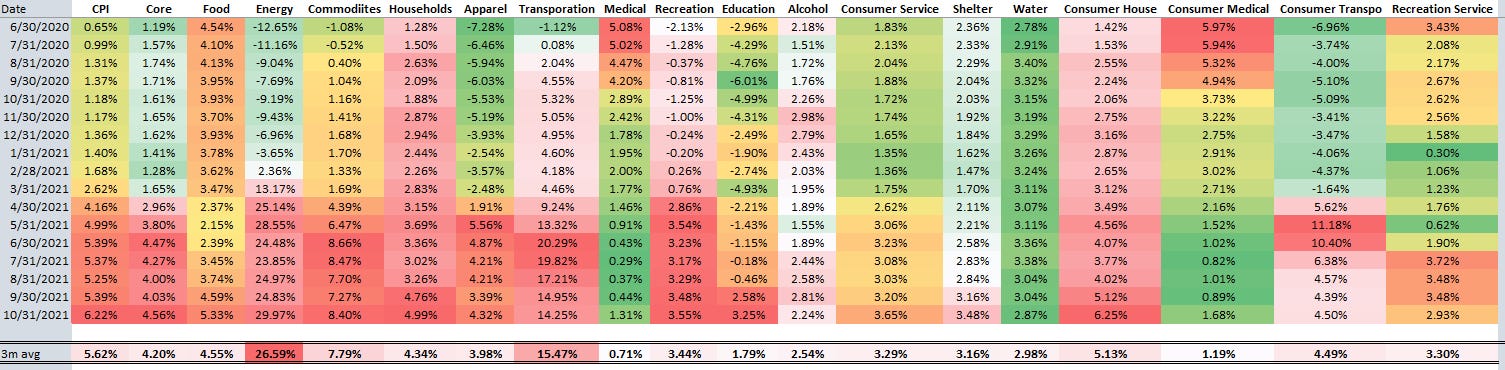

US Inflation came out 6.2% vs. 5.8% expected with Core Inflation at 4.6% vs. 4.3% expected.

Australia Unemployment Rate was reported 5.2% vs. 4.8% expected.

GB GDP Growth Rate YoY Prel. Q3 came lower at 6.6 vs. 6.8 expected.

US Michigan Consumer Sentiment Prel. Nov. edged lower to 66.8 vs. 72.4 expected.

US JOLTs Sep. also got lower at 10.44MM vs. 10.3MM from 10.63MM

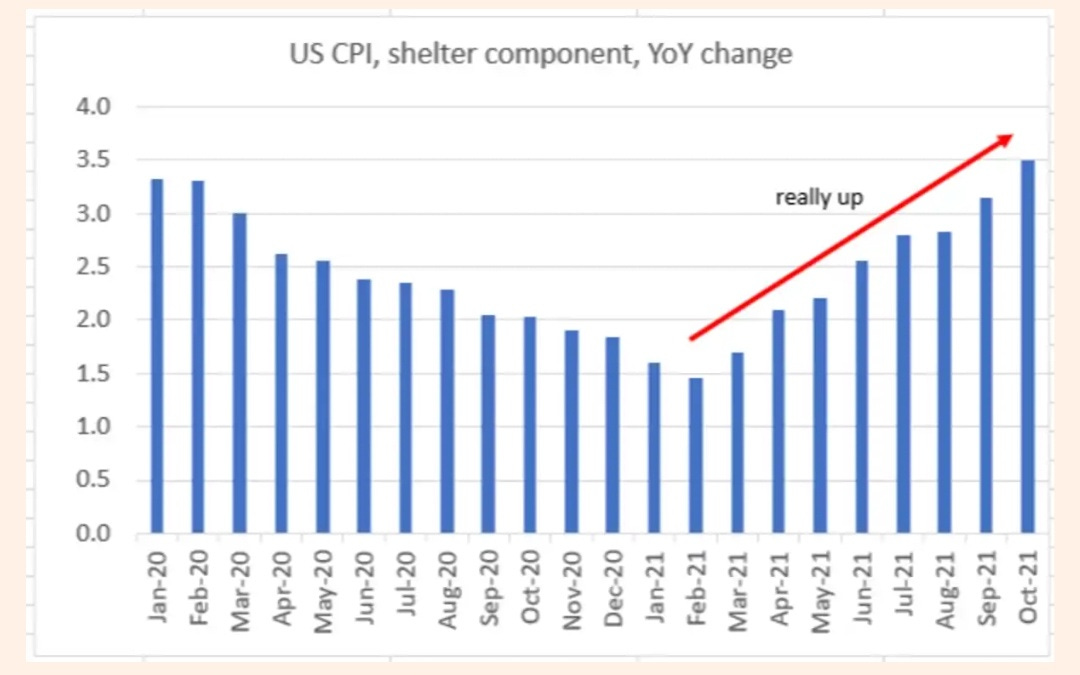

US CPI Decomposition:

[[Interesting Analysis]]:

-- FT

[[Important News]]: US Treasury secretary Janet Yellen said controlling Covid-19 was key to taming inflation, as Joe Biden’s administration tries to stop rising prices derailing the US economic recovery and the president’s legislative agenda. “The pandemic has been calling the shots for the economy and for inflation,” Yellen said, speaking on CBS’s Face the Nation programme. “And if we want to get inflation down, I think continuing to make progress against the pandemic is the most important thing we can do.” -- FT

[[Interesting Analysis]]: “Central banks were less hawkish than the markets were expecting them to be last week so we are seeing real yields going further down into negative territory,” Lale Akoner, BNY Mellon Investment Management senior market strategist, said on Bloomberg Television. The reflation trade is coming back again and the market is pricing in “a mid-cycle environment,” she said. -- Bloomberg

[[Important News]]: In a closely watched monthly market report, OPEC said global demand for oil would grow by 5.7 million barrels a day this year, 160,000 barrels a day less than it expected last month. The revision means the oil-producers group now expects demand for oil in 2021 to total 96.4 million barrels a day. Soaring fuel costs amid a global energy crunch were showing signs of weighing on demand. Weaker than expected demand for oil in China and India was now likely, OPEC said. In China, fresh outbreaks of Covid-19 cases and lockdowns, coupled with weaker factory activity and power outages have also reduced demand for fuels. -- WSJ

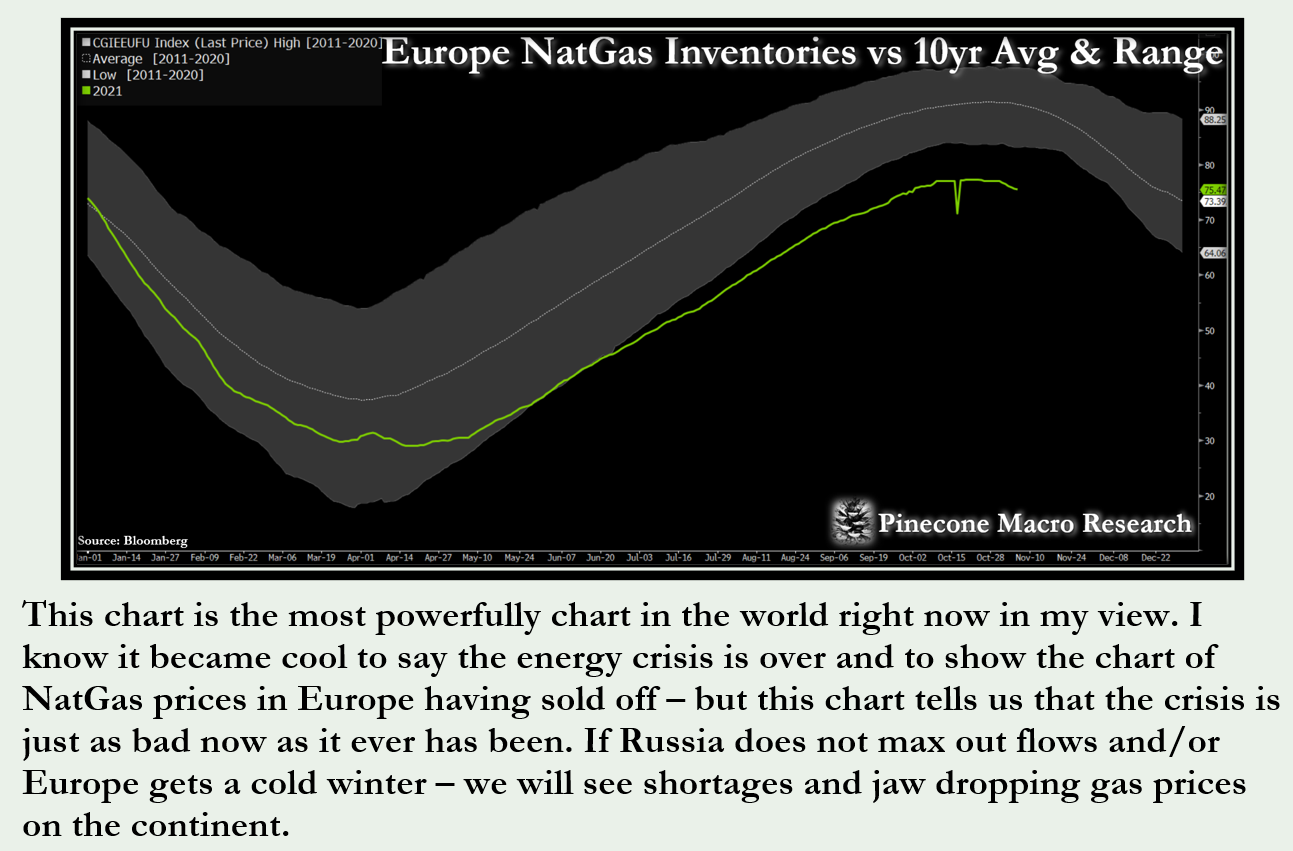

[[Interesting Analysis]]: We expect Brent prices will remain near current levels for the rest of 2021, averaging $82/b in the fourth quarter of 2021. In 2022, we expect that growth in production from OPEC+, U.S. tight oil, and other non-OPEC countries will outpace slowing growth in global oil consumption and contribute to Brent prices declining from current levels to an annual average of $72/b. The Henry Hub spot price will average $5.53/MMBtu from November through February in our forecast and then generally decline through 2022, averaging $3.93/MMBtu for the year amid rising U.S. natural gas production and slowing growth in LNG exports

-- EIA

[[Interesting Analysis]]:

[[Interesting Analysis]]: There were $300 billion in exports from Chinese companies last month, just below the record seen in September and the 13th straight month of double-digit growth. Even with a faster-than-expected rise in imports, that took the trade surplus to an all-time high of almost $85 billion, government data released Sunday showed. Shipments to the European Union were at a record high, up 44% from the same month in 2020, as reopening economies and the upcoming holiday season drove demand. Purchases by U.S. companies and consumers were also strong, just off the record se in September. (Click here for the full story.)

-- Bloomberg Supply Lines Newsletter 08.11.2021

[[Important News]]: The trading climate in the $22tn US government bond market has become less hospitable, adding to choppy moves in securities that act as a foundation of the global financial system. Liquidity — the ease with which an investor can buy or sell an asset — has deteriorated in recent weeks, data show. [...] “This seems to be something that has got to be sending sort of a troubling signal to central bankers, because it is not fundamentally driven. There’s clearly some ‘position unwinds’ that are going on as we speak,” said Subadra Rajappa, head of US rates strategy at Société Générale. -- FT

Element Capital sustained a roughly $1bn loss last month, making the New York hedge fund run by Jeffrey Talpins one of the highest-profile victims of the October tumult across bond markets. [...] Among other funds to suffer was Chris Rokos’s $12.5bn-in-assets Rokos Capital, which lost about 18 per cent last month. London-based Crispin Odey, having risen more than 100 per cent this year at the start of October, lost some of those gains to end the month 59 per cent up. New York-based Alphadyne also lost money. -- FT

Computer-powered hedge fund group AQR Capital Management is to remove five partners from its ranks and trim its bond arm, continuing to retrench operations after several lean years for many systematic trading strategies. -- FT

[[Important News]]: Millennium Management, one of the world’s biggest hedge funds, is returning about $15bn to investors while also raising billions of dollars in a private equity-style format as it tries to build a longer-term, more stable asset base. -- FT

Coronavirus

Cases are exploding across Europe, but Hospitalizations are still at lower levels. Deaths are edging up. The worrying statistic is that the relative positive tests are rising as well. At the same time the vaccination rates seem to stagnate between 60 & 80%.

A study based on Israeli data showed waning immunity of the Pfizer-BioNTech vaccine -- The New England Journal of Medicine

Vaccine efficacy against Covid-19 was 91.3% (95% confidence interval [CI], 89.0 to 93.2) through 6 months of follow-up among the participants without evidence of previous SARS-CoV-2 infection who could be evaluated. There was a gradual decline in vaccine efficacy. Vaccine efficacy of 86 to 100% was seen across countries and in populations with diverse ages, sexes, race or ethnic groups, and risk factors for Covid-19 among participants without evidence of previous infection with SARS-CoV-2. Vaccine efficacy against severe disease was 96.7% (95% CI, 80.3 to 99.9). In South Africa, where the SARS-CoV-2 variant of concern B.1.351 (or beta) was predominant, a vaccine efficacy of 100% (95% CI, 53.5 to 100) was observed. -- The New England Journal of Medicine

More News

[[Important News]]: Western intelligence suggests a “high probability of destabilisation” of Ukraine by Russia as soon as this winter after Moscow massed more than 90,000 troops at its border, according to Kyiv’s deputy defence minister. [...] Putin told state television at the weekend that Moscow was concerned about unannounced Nato drills in the Black Sea involving a “powerful naval group” and planes carrying strategic nuclear weapons, which he said presented a “serious challenge” for Russia. -- FT

NATO must take "concrete steps" to resolve the migrant crisis on the Belarus border, the Polish prime minister was quoted as saying on Sunday, adding that Poland, Lithuania and Latvia may ask for consultations under the alliance's treaty. -- Reuters

General Electric announced plans on Tuesday to split into three global public companies: Aviation: Helping customers achieve greater efficiency and sustainability and invent the future of flight. Healthcare: Driving innovation in precision health to address critical patient and clinical challenges (spinoff targeted for early 2023). Renewable Energy and Power: Supporting customers and communities seeking to provide affordable, reliable, and sustainable power (spinoff targeted for early 2024). -- Seeking Alpha

Next Week

Important PMI's for France, Germany, Europe and Great Britain incoming.

German Ifo Business Climate for November on Wednesday.

US Durable Goods, New Home Sales, Personal Income MoM, Personal Spending MoM and FOMC Minutes all on Wednesday.

German Consumer Confidence on Thursday and Inflation Rate YoY Prel. Nov on Friday.

Walmart, Target, Home Depot and Lowe's all scheduled to reports earnings and post guidance -- Seeking Alpha

U.S. President Joe Biden and Chinese counterpart Xi Jinping are expected to hold a virtual summit next week. -- Seeking Alpha

Regime

Currently the main problems for growth are the corona virus and the supply chain issues. The main problems for inflation is either a too harsh reaction of the central banks or a too small reaction. A comment on Inflation: While the fear of out-of-control inflation is probably over the top, it might be true that higher inflation levels might stay for a couple of years. That is due to a second round effect. The current inflation in energy and transportation is affecting especially companies. Companies are likely going to give those increases to the consumer next year in order to protect their margin. And this months CPI seems to point to the start of a more broad price increase. So while energy and transportation might relax, the damage has been done and is now sending a shockwave through the economy, which the consumer is probably feeling next year. The question is whether this years beginning wage talks are going to offset this. If they are too harsh, these increases in costs are likely to be passed on as well and then inflation might stay stronger than expected.

Scenario in one year

The market is currently pricing 2 rate hikes in the US and more Analysts are confident that while supply chain issues are still going to be there, they are less hurting in 2022. The main worry lies on how the current inflationary wave is going to be taken by the system. In such a scenario, essential companies with pricing power are beneficiaries. Companies in the cloud industry, in Infrastructure. Companies with less required products, more lifestyle products, are going to suffer more, examples likely being companies similar to Starbucks.

Trading

GLTR looks interesting.

Individual Chinese companies, such as JD.com could rebound.